Table of contents

- Is there a “right” place to invest ₹5–10 lakhs?

Step 1: Define your goal first

Step 2: Choose based on time horizon - Equity vs debt vs gold vs real estate

- Why not invest everything in one asset?

- Importance of asset allocation

- Why mutual funds could be a good starting point

- Sample allocation for ₹5–10 lakhs

- Consult a financial advisor or mutual fund distributor

- Connect with a mutual fund distributor on Moolaah

- Common mistakes investors make

- How to approach investing ₹5–10 lakhs in India?

“Invest and get rich.” “Buy this and get 10x returns.”

These are common messages investors come across on social media today.

While such claims may sound convincing, acting on them without context often leads to misaligned decisions — investing in assets that do not match your goals, time horizon, or risk tolerance.

When you have ₹5–10 lakhs to invest, the challenge is not lack of options — it’s choosing the right approach. From mutual funds and stocks to gold and real estate, there are multiple paths, but not all of them are suitable for every investor.

Focusing only on what is performing well “right now” can lead to short-term decisions that may not hold up over time.

Investing ₹5–10 lakhs, therefore, is not about finding the best-performing asset — it is about making structured decisions aligned with your financial goals.

This blog outlines a structured approach to investing ₹5–10 lakhs based on your financial objectives, time horizon, and risk tolerance.

Is there a “right” place to invest ₹5–10 lakhs?

It would’ve been easy if there was a single asset class that we could say with confidence will perform very well — and more importantly, everyone would be rich if that were the case.

So there is no single suggestable product or right place to invest 5-10 lakhs

More than return calculations, Investment decisions depend on:

- Why you are investing

- How long you can stay invested

- How much volatility you can handle

Two investors with the same amount may choose completely different allocations based on these factors.

Focusing on “where to invest” without context often leads to misaligned decisions. A more practical approach is to first define the purpose of the investment and then select suitable categories accordingly.

Step 1: Define your goal first

Before selecting any investment, the purpose of the money needs to be clear.

Common use cases include:

- Short-term needs (1–3 years)

- Medium-term goals (3–5 years)

- Long-term wealth creation (5+ years)

Without this clarity, investors may:

- Take higher risk than necessary

- Remain too conservative for long-term goals

- Switch investments frequently

The goal acts as the foundation for all further decisions. An investment meant for a vacation next year and one meant for retirement after 20 years cannot — and should not — be the same.

Step 2: Choose based on time horizon

The time horizon determines how much risk can be taken and which types of investments may be suitable.

Short-term horizon (up to 3 years)

The focus here is usually on capital preservation and liquidity.

For short-term goals such as emergency funds or planned expenses, exposure to high-risk assets like stocks or equity mutual funds is generally avoided due to potential volatility.

Commonly considered options include:

- Fixed deposits (FDs)

- Liquid mutual funds or money market funds

- Short-term debt funds or low-duration bonds

The objective is to preserve capital while earning modest, relatively stable returns.

Medium-term horizon (3–5 years)

This phase typically involves a balance between growth and stability.

For goals such as buying a vehicle, funding a major expense, or medium-term savings, a mix of asset classes may be considered to manage both risk and return.

Commonly considered options include:

- Hybrid or balanced mutual funds

- Debt funds or bonds

- Gold (physical gold or gold ETFs)

This approach allows for moderate growth while limiting excessive volatility.

Long-term horizon (5+ years)

For long-term goals such as retirement or wealth creation, investors generally have more time to manage market fluctuations.

This allows for a higher allocation to growth-oriented assets.

Commonly considered options include:

- Equity mutual funds or direct equity

- Long-term instruments such as Public Provident Fund (PPF) or National Pension System (NPS)

- Sovereign gold bonds

- Real estate or REITs (depending on suitability and liquidity needs)

Over longer periods, these investments have the potential to generate returns that can outpace inflation, though they come with higher short-term volatility.

Equity vs debt vs gold vs real estate

Different asset classes behave differently across market conditions. Instead of asking which one is “best,” it is more useful to understand what role each plays in a portfolio.

Equity

Equity is typically associated with long-term wealth creation.

- Higher return potential over long periods

- Higher short-term volatility

- Suitable for investors with a longer time horizon

Equity investments, including stocks and equity mutual funds, have historically delivered higher returns compared to other asset classes over extended periods. However, this comes with fluctuations that may not be suitable for short-term needs.

Debt

Debt instruments are generally used for stability and predictable outcomes.

- Lower volatility compared to equity

- Relatively stable return expectations

- Suitable for capital preservation and income generation

Examples include bonds, fixed deposits, and debt mutual funds. These are often considered when the priority is to protect capital rather than maximise growth.

Gold

Gold is commonly used as a diversification asset rather than a primary investment.

- Acts as a hedge during inflation or uncertainty

- Performance may differ from equity and debt cycles

- Moderate risk compared to other asset classes

Gold does not generate income like interest or dividends but may help balance overall portfolio risk during certain market conditions.

Instead of buying physical gold, which may involve additional costs such as GST, making charges, and storage concerns, investors today have more efficient alternatives.

Gold can be accessed through financial instruments such as:

- Sovereign Gold Bonds (SGBs), which may be suitable for investors comfortable holding for the long term

- Gold ETFs, which offer flexibility to buy and sell on exchanges when liquidity is required

These options help reduce some of the practical limitations associated with physical gold while providing exposure to the asset.

Real estate

Real estate is a widely used asset class but comes with specific constraints.

- Requires relatively high capital

- Lower liquidity compared to financial assets

- May offer rental income and long-term appreciation

For many investors, direct real estate investment may not always be flexible due to large ticket size and longer holding periods.

At the same time, there are now more accessible ways to participate in real estate through financial instruments such as Real Estate Investment Trusts (REITs).

These allow investors to gain exposure to real estate assets without directly purchasing property, typically with lower capital requirements and relatively better liquidity compared to physical real estate.

Gold vs equity vs real estate vs debt – 20-year return comparison

| Asset Class | Approx. 20-Year CAGR |

| Gold | ~15% |

| Equity (Nifty 50 TRI) | ~13.5% |

| Real Estate | ~7.8% |

| Debt | ~7.6% |

Source: Times Now (Dec 2025 report)

Although gold has outperformed other asset classes over certain periods, no single asset class consistently outperforms others across all timeframes.

Each behaves differently depending on economic conditions, interest rates, and market cycles.

This is why, instead of choosing between equity, debt, gold, or real estate, investors often consider how these asset classes can work together within a broader allocation.

Why not invest everything in one asset like gold or silver?

One of the most discussed topics recently has been the sharp rise in gold and silver prices.

Looking at recent performance, the returns can appear extremely attractive:

Gold and silver returns in 2025 (MCX prices)

| Asset | Price on Jan 1, 2025 | Price on Dec 31, 2025 | 1-Year Return |

| Gold | ₹76,308 | ₹1,32,640 | 73.82% |

| Silver | ₹85,913 | ₹2,29,452 | 167.07% |

Along with this, gold has also delivered strong returns over longer periods, including over a 20-year timeframe.

At first glance, such returns may make it seem logical to invest heavily — or even entirely — in the asset that is currently performing well.

However, this is where most investors make a mistake.

Short-term performance does not always translate into long-term consistency.

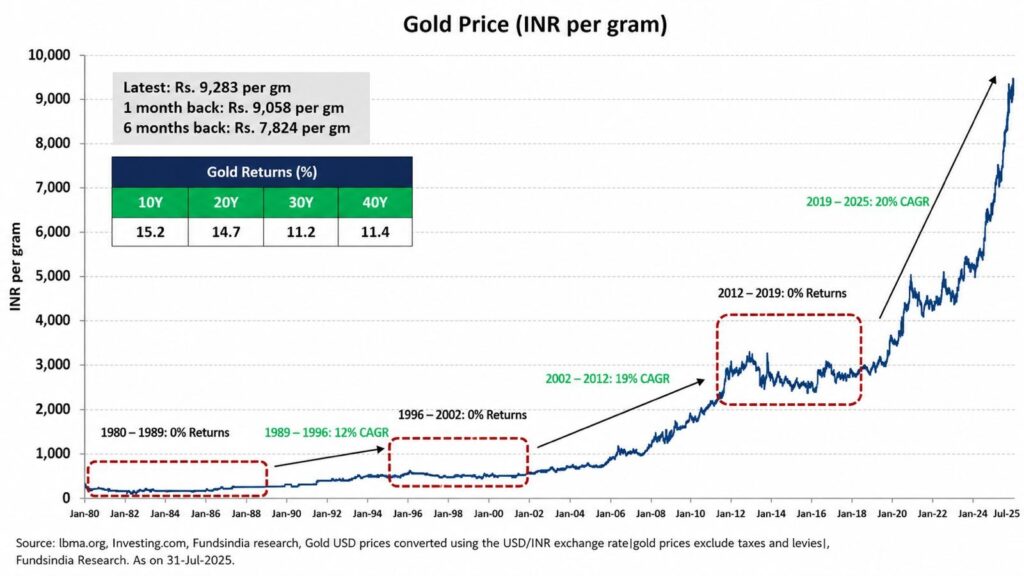

Gold price in India (1980–2025)

Source: FundsIndia (Aug 2025 report)

For example, between 2012 and 2019, gold prices remained relatively flat, delivering minimal returns over that period. Investors who entered during earlier highs had to wait several years to see meaningful gains.

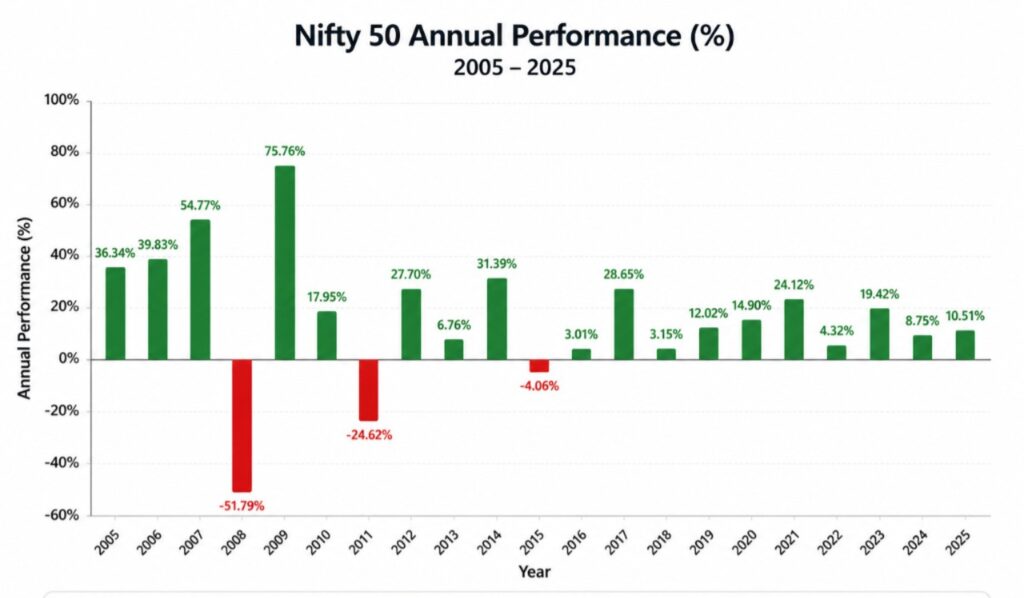

Let’s also look at the 20-year performance of the Nifty 50 (2005–2025).

Source: Primeinvestor

Over this period, returns have ranged from as high as +75.76% to as low as –51.79% in a single year.

This highlights a key reality:

Different asset classes follow different return patterns — some show long-term growth with volatility, while others may remain flat for years and move sharply during specific periods.

- Gold may rally sharply during uncertainty

- Equity may outperform during growth phases

- Debt may provide stability during volatility

Relying entirely on one asset class exposes your investment to timing risk, where outcomes depend heavily on when you invest.

A more balanced approach across asset classes helps reduce this dependency and creates more consistency over time.

Importance of asset allocation

Based on the performance of different asset classes, one thing becomes clear — it is difficult to predict which asset class will perform well in the near term.

What investors can control, however, is how their money is distributed across different asset classes.

This is where asset allocation becomes important.

Instead of relying on a single asset to deliver returns, spreading investments across categories such as equity, debt, and gold helps reduce the impact of poor performance in any one area.

A structured allocation helps:

- Reduce the risk of significant losses from one asset class

- Manage volatility across market cycles

- Align investments with time horizon and risk tolerance

Rather than trying to maximise returns from a single investment, asset allocation focuses on building a more stable and consistent investment approach over time.

Why mutual funds could be a good starting point?

For many investors, especially those starting out or managing moderate amounts like ₹5–10 lakhs, implementing asset allocation independently can be challenging.

Direct stock investing requires:

- Selecting individual companies

- Tracking performance regularly

- Understanding market movements and financial data

Without sufficient time or experience, this can lead to inconsistent decisions or concentration in a few stocks.

To simplify this, mutual funds can be considered as a starting point.

Mutual funds pool money from multiple investors and invest across a diversified set of securities, managed by professional fund managers.

Based on the type of fund, investors can access different types of mutual funds:

- Equity mutual funds for long-term growth

- Debt mutual funds for stability and income

- Hybrid funds for a mix of growth and stability

This structure allows investors to participate in markets without needing to manage individual investments directly.

Sample allocation for ₹5–10 lakhs

There is no single “correct” allocation for ₹5–10 lakhs. The allocation should be based on your time horizon and ability to handle risk.

Below are a few simplified scenarios aligned with different time horizons:

Short-term horizon (up to 3 years)

Suitable for goals such as emergency funds, planned expenses, or near-term requirements.

Example allocation (₹10 lakhs):

- 70–80% Debt (FDs, liquid funds, short-term debt funds) → ₹7,00,000–₹8,00,000

- 10–20% Cash / liquid options → ₹1,00,000–₹2,00,000

- Minimal or no equity exposure

The focus here is on capital preservation and liquidity, rather than return maximisation.

Medium-term horizon (3–5 years)

Suitable for goals such as purchasing a vehicle, funding a major expense, or medium-term savings.

Example allocation (₹10 lakhs):

- 40–60% Equity / hybrid funds (equity mutual funds, hybrid/balanced funds) → ₹4,00,000–₹6,00,000

- 30–40% Debt (debt mutual funds, bonds, fixed deposits) → ₹3,00,000–₹4,00,000

- 10–15% Gold (physical gold/gold ETFs) → ₹1,00,000–₹1,50,000

This approach balances growth and stability, allowing moderate participation in equity while managing downside risk.

Long-term horizon (5+ years)

Suitable for goals such as retirement or long-term wealth creation.

Example allocation (₹10 lakhs):

- 60–75% Equity (equity mutual funds, direct equity) → ₹6,00,000–₹7,50,000

- 10–20% Debt (PPF, NPS, long-term debt funds, bonds) → ₹1,00,000–₹2,00,000

- 10–15% Gold / REITs (Sovereign Gold Bonds /gold ETFs, REITs) → ₹1,00,000–₹1,50,000

Here, the focus is on growth, with the understanding that short-term volatility is part of long-term investing.

These examples are indicative and meant to show how allocation can change based on time horizon. The actual mix may vary depending on your financial situation, existing investments, and comfort with market fluctuations.

Consult a financial advisor for comprehensive financial planning

The asset allocation examples given above are only indicative and may not fully reflect your specific financial needs. Also, only qualified professionals are permitted to suggest specific products or funds based on an individual’s financial situation.

When investing a relatively large amount such as ₹5–10 lakhs, having the right guidance can help bring clarity and structure to your decisions.

It is also important to avoid relying on random online tips, as they are not tailored to your goals, time horizon, or risk tolerance.

If you are looking for comprehensive financial planning, consulting a qualified, SEBI-registered financial advisor may be useful. A financial advisor can help:

- Understand your financial situation, goals, and time horizon

- Assess your risk tolerance

- Create a structured investment plan

- Guide you through portfolio construction and periodic review

This can help you stay aligned with your plan, especially during market volatility or when adjustments are required over time.

Consult a mutual fund distributor for mutual fund investing

If your focus is primarily on mutual fund investments, you may consider working with an AMFI-registered mutual fund distributor.

A mutual fund distributor can help:

- Explain different mutual fund options and assist in selecting funds aligned with your financial objectives

- Facilitate investments in mutual funds

- Assist with transaction execution and documentation

- Support ongoing tracking and portfolio reviews

Seeking guidance from certified professionals can help you avoid common mistakes and build a portfolio with a more structured asset allocation. It also ensures you have support during periods of market uncertainty or when changes are needed.

To learn how to invest through a mutual fund distributor, read “Step-by-step process to start investing with a mutual fund distributor”

Connect with a mutual fund distributor on Moolaah

If you’re planning to invest in mutual funds and want to find a suitable mutual fund distributor, Moolaah can help simplify the process.

Through Moolaah, you can:

- Access a verified list of mutual fund distributors

- Connect with a distributor based on your requirements

- Discuss your financial objectives and investment preferences

- Select and invest in funds suggested by your mutual fund distributor

- Track and manage your portfolio through a single platform

- Invest across multiple products including mutual funds, fixed deposits, bonds and more.

This helps reduce reliance on fragmented information and supports a more organised investment process.

Explore verified mutual fund distributors on Moolaah

Common mistakes investors make

Even with the right information and multiple investment options available, certain common mistakes can affect outcomes when investing a large amount like ₹5–10 lakhs.

1. Investing based on recent performance

Choosing investments based on what has performed well recently often leads to poor entry decisions. Markets and asset classes move in phases, and past short-term performance does not guarantee future outcomes.

2. Ignoring asset allocation

Putting the entire amount into a single category increases concentration risk. Without diversification, the portfolio becomes highly dependent on the performance of one asset class.

3. Not considering existing investments

New investments should complement your current portfolio, not duplicate exposure. Ignoring existing allocations can lead to overexposure in certain asset classes without realising it.

4. Making frequent changes

Frequent switching can:

- Increase transaction costs

- Create unnecessary tax impact

- Disrupt long-term consistency

Constantly reacting to market movements often leads to decisions that are not aligned with long-term goals.

5. Trying to invest without proper guidance

Relying solely on social media tips or unverified sources can lead to decisions that are not aligned with your financial goals or risk tolerance. These suggestions are often general and not tailored to individual situations.

Seeking guidance from qualified professionals can help bring structure, clarity, and consistency to your investment decisions.

How to approach investing ₹5–10 lakhs in India?

Investing ₹5–10 lakhs is not about identifying a single opportunity — it is about building a structured allocation that aligns with your financial situation.

Decisions based on goals, time horizon, and risk tolerance tend to be more consistent than those driven by short-term market movements or trends.

Instead of trying to predict which asset will perform best, focus on creating a balanced approach that can adapt across different market conditions.

Where needed, seeking guidance from qualified professionals can help bring clarity to your decisions, ensure better alignment with your financial objectives, and provide support during market volatility.

A disciplined and structured strategy, supported by the right guidance, not only reduces uncertainty but also helps you stay consistent over time — which is often more important than chasing higher returns.

FAQs

Where should I invest ₹5–10 lakhs in India right now?

There is no single best option. The right investment depends on your goals, time horizon, and risk tolerance.

How should I allocate ₹10 lakhs across different investments?

Allocation should be based on time horizon — short-term focuses on stability, while long-term allows higher equity exposure.

Is equity suitable for investing ₹5–10 lakhs?

Equity may be suitable for long-term goals, but it involves short-term volatility and is not ideal for near-term needs.

Should I invest ₹10 lakhs as a lump sum or in phases?

Both approaches are used. The choice depends on your comfort with market timing and volatility.

Is gold a good investment for ₹5–10 lakhs?

Gold is typically used for diversification, not as a primary investment.

What is the biggest mistake when investing ₹5–10 lakhs?

Focusing only on recent performance instead of goals and time horizon.

Why is asset allocation important for ₹5–10 lakh investments?

It reduces risk by spreading investments across different asset classes instead of relying on one.

Can I invest ₹5–10 lakhs without professional guidance?

Yes, but lack of structure or relying on unverified tips can lead to poor decisions.

How can a mutual fund distributor help with ₹10 lakh investment?

They assist with fund selection, execution, and tracking based on your financial needs.

How does Moolaah help investors invest ₹5–10 lakhs?

Moolaah connects you with verified mutual fund distributors and helps manage investments in one place.

Disclaimer: Moolaah is an AMFI-registered Mutual Fund Distributor (ARN-245875). We distribute Regular Plans of Mutual Fund schemes, which involve the payment of trail commission to us. Our services are incidental to product distribution and do not constitute independent investment advice. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.